Cultural leaders and cultural institutions are key influential figures and bodies that not only lead subjects but also urge people to adopt development initiatives and practices to improve their livelihoods.

In appreciation of their influence and leadership, subjects and well-wishers usually make contributions to assist cultural institutions to navigate their administrative operations.

The Institution of Traditional or Cultural Leaders Act, 2011 defines a traditional or cultural leader as a king, or similar traditional or cultural leader, by whatever name called, who derives allegiance from the fact of birth or descent in accordance with the customs, traditions, usage or consent of the people led by that leader.

The Act further defines a traditional or cultural leader as the throne, station, status or other position held by a traditional or cultural leader.

These leaders and institutions enjoy privileges or benefits under Section 10 of the Institution of Traditional or Cultural Leaders Act, 2011 from the government that are free from income tax such as: official and support vehicles, educational allowance for two biological children up to university level within Uganda, travel by first class with their spouse once a year, contribution from government upon death, security for the traditional leader and their family, contribution by government towards rehabilitation of residence, maintenance of cultural sites to a standard determined by the ministry responsible for culture among others.

In addition, gifts or donations received by cultural leaders or institutions may benefit from exemption from income tax under Section 21(1)(j) of the Income Tax Act that exempts the value of any property acquired by gift, bequest, devise, or inheritance that is not included in business, employment, or property income.

For an item of property to qualify as a gift, it must be given voluntarily without expectation of a reward and must be accepted by the recipient.

The person giving the gift or donation is expected to account for taxes, where applicable, on the donation.

For instance, where the gifts or donations are given by business entities, the entity making the donation is expected to account for taxes applicable on the donation.

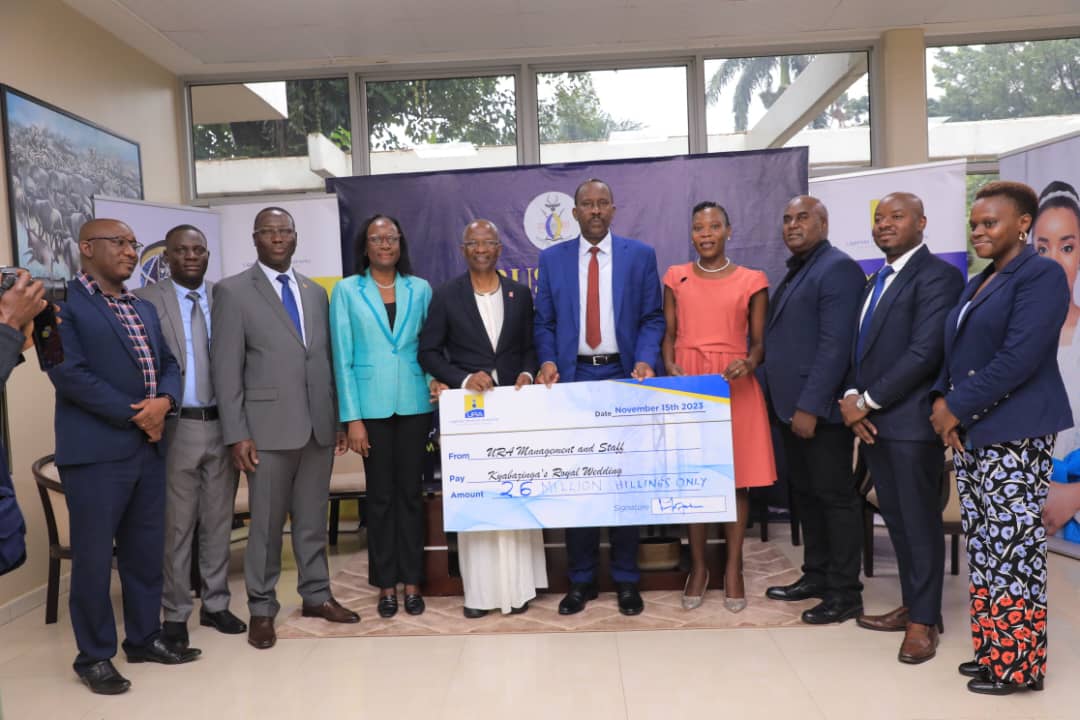

For example, if XYZ Hardware Limited donates 100 bags of cement that it had procured for its business activities to a cultural leader, XYZ Hardware Ltd will be expected to account for value added tax on the supply and will not be able to deduct the expense for income tax purposes.

“If a cultural institution has a real-estate business that employs and earns income or property income from its activities, then this agency and other similar income generating entities are required to meet their tax obligations since their services are not entirely charitable,” Ibrahim K. Bbossa the URA spokesperson clarified.

In the same spirit, an individual who makes a donation to a constitutionally recognized cultural or traditional leader is supposed to account for the taxes applicable, even if the recipient – the cultural leader is exempt.

“A good illustrative example is if an entity like a telecommunication company that deals in VAT-able services or goods decided to donate a service or goods to a kingdom, the VAT tax obligations have to be accounted for by the donor entity,” Bbossa added.

This simply means that the donor becomes the final consumer and must then file and pay the taxes due to that donation they made because VAT is a final consumer tax and the cultural leader or institution in this case will be exempt from paying those taxes.

{kind=link}